ETH Restaking Protocols: A Research Guide

Ethereum restaking protocols in 2026 — Ether.fi, Renzo, Kelp DAO, Puffer, Swell — compared on live TVL, AVS exposure, slashing risk, and real yield. Includes the April 2026 Kelp $292M bridge exploit.

Table of contents

- Why restaking matters in 2026

- Top 5 ETH restaking protocols in 2026

- Ether.fi — deep dive

- Kelp DAO — deep dive

- Puffer Finance — deep dive

- Renzo — deep dive

- Swell — deep dive

- How LRTs actually differ from LSTs

- Best ETH restaking protocol by use case

- How to actually evaluate an LRT before you deposit

- Realistic LRT portfolio (May 2026)

- Risk summary

- The brutal truth about LRTs

- Looking ahead to 2027

Why restaking matters in 2026

The April 2026 Kelp DAO $292M bridge exploit — 2026's largest DeFi theft — triggered sector-wide contagion that collapsed Renzo, Puffer, and Swell TVL by 80–95%; only Ether.fi ($3.8B) held ground; the incident exposed cross-chain bridge risk as a third attack surface distinct from slashing or smart-contract bugs. Last verified: 2026-05-27.

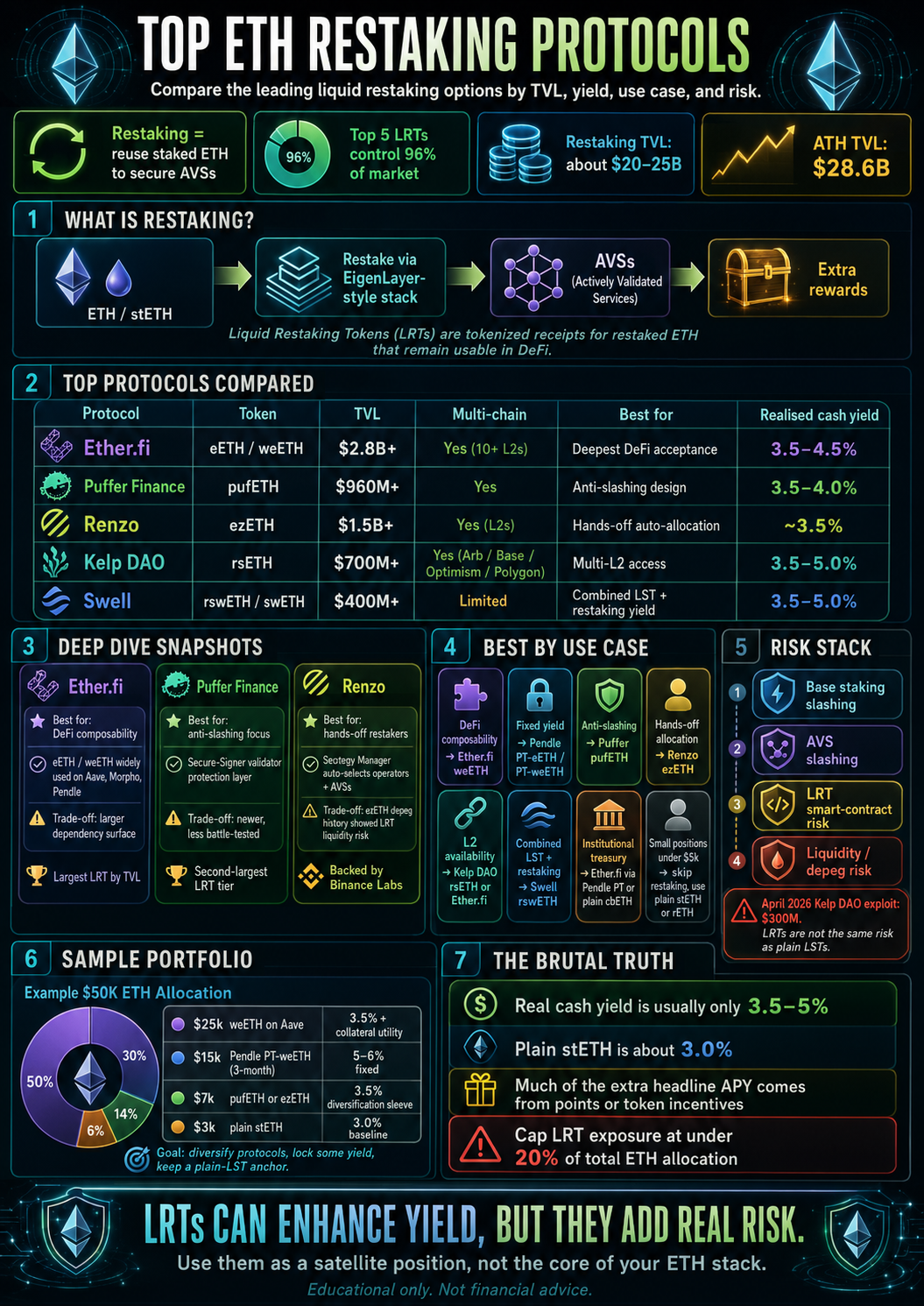

Ether.fi leads with $3.8B TVL as of May 2026 (DefiLlama live). EigenLayer (EigenLayer is the protocol that pioneered restaking, letting staked ETH secure additional services called AVSs) peaked at $18B+ TVL in early 2026 before contracting to ~$8.9B by March 2026, with further declines after the Kelp contagion event. Five LRT (LRT = liquid restaking token, a tokenised receipt for restaked ETH usable as DeFi collateral) protocols — Ether.fi, Kelp, Renzo, Puffer, Swell — once controlled 96% of the market; that concentration has not changed, but the second-through-fifth tiers are a fraction of their former size.

The defining event of 2026 was the April 18 Kelp DAO $292M LayerZero bridge exploit (see full breakdown in the Kelp section below). It was 2026's largest DeFi theft, attributed to North Korea's Lazarus Group (TraderTraitor subunit). rsETH operations were restored on May 26, 2026 — five weeks after the attack — following a coordinated recovery including a $161M ETH buyback by DeFi United and freezing of 30,766 ETH by the Arbitrum Security Council. If you only remember one thing from this guide: LRT risk is not just slashing and smart contracts. The bridge and cross-chain infrastructure layer is a material attack surface.

ETH restaking protocols compared — LRT market share, yield, best use cases, risk stack, and a sample ETH allocation. TVL figures as of May 27, 2026.

Top 5 ETH restaking protocols in 2026

Ether.fi ($3.8B, dominant), Kelp DAO ($1.35B, recovering), Renzo ($163M, collapsed), Puffer ($59M, collapsed), Swell ($29M, collapsed) — the April 2026 contagion event permanently re-sorted the category. Last verified: 2026-05-27.

| Protocol | Token | TVL (May 27, 2026) | Multi-chain | Best for |

|---|---|---|---|---|

| Ether.fi | eETH / weETH | $3.8B | Yes (10+ L2s) | DeFi composability, broad acceptance |

| Kelp DAO | rsETH | $1.35B | Yes (Arb/Base/Optimism/Polygon) | Recovering post-exploit; monitor before depositing |

| Renzo | ezETH | ~$163M | Yes (L2s) | Hands-off auto-allocation; TVL severely contracted |

| Puffer Finance | pufETH | ~$59M | Limited | Anti-slashing tech; TVL severely contracted |

| Swell | rswETH / swETH | ~$29M | Limited | Combined LST+restaking; TVL severely contracted |

TVL sources: DefiLlama live data (defillama.com). Figures reflect post-Kelp-exploit contraction across the sector.

Ether.fi — deep dive

Ether.fi — deep dive

Full guide: ether.fi.

Ether.fi is the only LRT with DeFi acceptance approaching a real LST, and the only major LRT whose TVL held through the April 2026 contagion event.

Best for

ETH holders who want the most DeFi-accepted LRT. eETH and weETH (weETH is the wrapped, non-rebasing version of Ether.fi's eETH, used as collateral across DeFi) are listed on Aave, Morpho, Pendle, Curve, and Balancer with deep liquidity. If you want to actually use the LRT as collateral, this is the only top-5 LRT where that is frictionless post-April 2026.

How it actually works

Deposit ETH → Ether.fi runs the validator → you receive eETH (rebasing). Wrap to weETH for DeFi composability. The non-custodial design means depositors retain validator keys (via "NodeOperators-as-a-Service"), an unusual structure that contrasts with Renzo and Kelp's pooled-operator models. Restaking is routed through EigenLayer, with AVS allocation managed by the Ether.fi DAO. After the April 2026 Kelp exploit, Ether.fi strengthened its cross-chain security and froze its LayerZero OFT bridge as a precaution while reviewing its own bridge architecture.

Audit history and trust

Multiple audits via Certik, Halborn, Solidified. $3.8B TVL (DefiLlama, May 2026) makes it by far the largest LRT, holding ground through the April contagion. No protocol-level loss to date. ETHFI governance token trades at ~$0.38 (May 2026), down from an $8.53 ATH in March 2024.

Yield

Base ETH staking ~3.0–3.4% + restaking rewards 0.5–1.5% + ETHFI token incentives. Realised cash yield ~3.5–4.5%.

The bear case

Largest surface area also means largest target. Ether.fi opts into the most AVSs of any LRT (10+), meaning each new AVS slashing condition is inherited by every weETH holder. EigenLayer slashing went live April 17, 2025, but no live slash events have yet occurred on any operator (through May 2026). That record can change without warning.

Kelp DAO — deep dive

Kelp DAO — deep dive

The April 18, 2026 $292M bridge exploit is the category's most consequential security incident to date; rsETH is operationally restored as of May 26, 2026, but depositors must make their own assessment of trust after a five-week suspension of withdrawals.

The April 2026 exploit — what actually happened

On April 18, 2026 at 17:35 UTC, attackers (attributed by LayerZero to North Korea's Lazarus Group / TraderTraitor subunit) drained 116,500 rsETH — approximately $292 million from Kelp's LayerZero-powered cross-chain bridge. This was not a withdrawal-logic smart-contract bug. It was an attack on off-chain infrastructure:

- Kelp's bridge used a 1-of-1 DVN (Decentralized Verifier Network) setup — a single LayerZero Labs verifier node was the sole source of cross-chain message validation.

- Attackers compromised two internal LayerZero RPC nodes and simultaneously DDoS'd external nodes, isolating the single verifier.

- The poisoned nodes reported phantom rsETH burns on the source chain (Unichain) that never occurred. The Ethereum-side contract — seeing what appeared to be a valid verified message — released 116,500 real rsETH to attacker-controlled addresses.

- Kelp's emergency-pause multisig froze contracts 46 minutes later (18:21 UTC), blocking a follow-up $95M attempt. The Arbitrum Security Council froze 30,766 ETH the attacker held on Arbitrum One.

The blame was disputed: Kelp said LayerZero's default 1-of-1 DVN configuration was the root cause; LayerZero said Kelp chose this setup; LayerZero itself later acknowledged it had approved the configuration. As of May 5, 2026, the dispute remained unresolved in public statements.

Recovery

rsETH depegged sharply on secondary markets (to ~0.85 ETH at trough). DeFi United raised $161M in ETH from 14 contributors to support a buyback that helped rsETH recover to ~0.97 ETH. Kelp completed the final tranche of the rsETH recovery plan on May 26, 2026 — sending 20,373.7 rsETH to the LayerZero lockbox — and rsETH mints, redemptions, and rewards are operational again. Kelp is migrating cross-chain infrastructure from LayerZero to Chainlink CCIP. Aave rsETH markets have also reopened.

Post-exploit assessment

Kelp still has $1.35B in TVL (DefiLlama), much of it from pre-exploit depositors who held through recovery. Whether that reflects conviction or trapped capital is unclear. Do not deposit into Kelp without reading the full post-mortem, confirming the CCIP migration timeline, and deciding whether you accept the residual trust deficit. The multi-chain LRT thesis is intact — the specific bridge implementation failed, not the concept.

Best for (post-recovery)

Multi-chain rsETH access across Arbitrum, Base, Optimism, Polygon — if and when you are satisfied with the revised security architecture.

Yield

Base staking + restaking rewards + KEP token incentives. Cash yield ~3.5%. Monitor closely as operations normalise.

Puffer Finance — deep dive

Puffer Finance — deep dive

Puffer designed for AVS slashing risk from day one, but post-April 2026 contagion TVL has contracted to approximately $59M — a more than 90% decline from its ~$850M+ peak.

Best for

Restakers who care about anti-slashing tech at the validator level. Puffer's "Secure-Signer" design adds a slashing-protection layer at the validator: node operators cannot sign slashable messages even if their keys are compromised, which materially reduces worst-case scenarios with unaudited AVSs. Anchorage Digital partnered with Puffer in early 2026 for institutional pufETH custody access.

Trade-offs

At $59M TVL, Puffer faces a liquidity credibility problem. Thin secondary markets for pufETH widen the exit discount in stress. If institutional interest via the Anchorage integration converts to meaningful inflows, TVL could recover — but the post-April 2026 cohort will need evidence of sustained deposits before pufETH regains its prior standing.

Audit history and trust

Audited by Sigma Prime, Certora, Quantstamp. No Puffer-specific exploit to date — TVL decline was contagion-driven, not a protocol failure.

Yield

Base staking + restaking + PUFFER token rewards. Realised cash yield ~3.5–4%.

Renzo — deep dive

Renzo — deep dive

ezETH's April 2024 sell-off after Renzo's airdrop allocation announcement remains the canonical LRT depeg case study; TVL collapsed from a $3B+ peak to ~$163M by May 2026 following the April contagion event.

Best for

Hands-off restakers who want a "Strategy Manager" that auto-selects operators and AVSs based on risk-adjusted return. If you don't want to think about which AVSs to opt into, Renzo decides for you.

The April 2024 ezETH depeg — numbers corrected

ezETH dropped to approximately $688 on Uniswap in April 2024 when Renzo's airdrop allocation announcement triggered concentrated exits. At the time ETH was trading at roughly $3,100, implying a depeg of roughly 78% relative to par — not the "$0.74" figure cited previously, which was a price unit confusion. The collapse cascaded through Balancer and Gearbox pools, liquidating more than 250 users for roughly $56M in losses in under an hour. The protocol itself did not fail; secondary market liquidity failed under the forced selling. Anyone using ezETH as leveraged collateral got liquidated.

TVL collapse

Renzo peaked at $3B+ TVL in early 2026. Post-April 2026 contagion, TVL stands at ~$163M (DefiLlama). The REZ community voted on buybacks (Proposal RP-6A, executed October 2025 with a 1.05% supply test burn) but this has not materially reversed TVL attrition.

Audit history and trust

Audited by Halborn, Code4rena, Pashov. Backed by Binance Labs. No Renzo-specific exploit — TVL decline is contagion-driven.

Yield

Combines all yield sources into a single ezETH balance. Realised cash yield ~3.5%.

Swell — deep dive

Swell — deep dive

Swell's rswETH TVL stands at ~$29M (DefiLlama, May 2026), down from a $374M peak, reflecting the same sector-wide contagion. The combined LST+restaking (swETH + rswETH) product thesis remains intact architecturally; the scale has not.

Best for

ETH holders who want base staking + restaking yield in one token, with Swell's L2 ambitions providing additional upside optionality. Limited multi-chain deployment vs Ether.fi or the pre-exploit Kelp.

Yield

10% fee split evenly between node operators and treasury. Realised cash yield ~3.0–3.5%.

How LRTs actually differ from LSTs

An LRT is an LST plus a stack of additional smart-contract, slashing, and cross-chain bridge risks; the yield premium is 50–150bps; the risk premium is not small.

| Plain LST (stETH) | LRT (weETH) | |

|---|---|---|

| Underlying | ETH staked via Lido | ETH staked + restaked via EigenLayer |

| Smart-contract layers | Lido + Ethereum staking | Ether.fi + EigenLayer + each AVS |

| Bridge/infra risk | Minimal | Material — Kelp exploit proved this |

| Slashing conditions | Ethereum consensus only | Ethereum consensus + every opted-in AVS |

| Cash yield 2026 | 3.0–3.4% | 3.5–4.5% |

| Historical max depeg | 0.935 ETH (stETH, Jun 2022) | ~0.78 ETH (ezETH vs ETH, Apr 2024) |

| Largest historical loss | None (protocol-level) | $292M (Kelp bridge, Apr 2026) |

| DeFi acceptance | Universal | Deep only for Ether.fi weETH |

| Time to exit in stress | Hours (Curve) | Days–weeks (queue + potential freeze) |

The yield premium for taking on LRT risk over plain LST is roughly 50–150bps in cash terms. The Kelp exploit proved that bridge and infra risk can equal or exceed AVS slashing risk in practice — something most LRT risk models did not adequately price before April 2026.

Best ETH restaking protocol by use case

DeFi composability: Ether.fi weETH. Fixed yield: Pendle PT-eETH. Anti-slashing: Puffer. Hands-off: Renzo. Multi-L2 (post-recovery): Kelp. Last verified: 2026-05-27.

- Best LRT for DeFi composability — Ether.fi eETH or weETH (most-accepted collateral; held through April 2026 contagion).

- Best LRT for fixed yield — Pendle PT-eETH or PT-weETH (lock yield 3–12 months, no restaking exposure).

- Best LRT for max anti-slashing tech — Puffer pufETH (Secure-Signer design), though liquidity is thin at current TVL.

- Best LRT for hands-off allocation — Renzo ezETH (Strategy Manager auto-routes), noting the dramatic TVL contraction.

- Best LRT for L2 availability — Ether.fi (most L2 deployments currently). Kelp is rebuilding cross-chain infra on Chainlink CCIP.

- Best LRT for combined LST+restaking — Swell rswETH (architecturally; not for liquidity depth at current scale).

- Best LRT for points farming — Whichever protocol has the most active points campaign at the time (track via DeFiLlama or Sonar); note ETHFI's trajectory as a reality check on airdrop upside.

- Best LRT for institutional treasury — Ether.fi via Pendle PT (locked yield + transferable PT) or direct Coinbase cbETH (LST-only, no restaking risk). Puffer via Anchorage for institutional pufETH custody.

- Best LRT for under $5,000 positions — Skip restaking entirely; use plain stETH or rETH. LRT smart-contract and bridge risk premium is not worth it at small size.

- Best LRT to avoid — Any LRT under 6 months old with under $50M TVL or no public audit reports; any LRT with a 1-of-1 DVN cross-chain configuration.

How to actually evaluate an LRT before you deposit

Four checks: bridge/infra architecture, contract surface area, AVS opt-in list, redemption queue, points-to-cash yield ratio. The Kelp exploit proved bridge security deserves the same scrutiny as smart contracts. Last verified: 2026-05-27.

- Audit the cross-chain bridge architecture first. The Kelp April 2026 exploit was not a smart-contract bug — it was a single-verifier LayerZero bridge configuration. Ask: how many independent verifiers sign cross-chain messages? Is there a second DVN or fallback? Kelp used 1-of-1; any LRT with similar exposure is unacceptable. After the exploit, Kelp is migrating to Chainlink CCIP and Ether.fi strengthened cross-chain security immediately. Treat bridge design as a first-order risk factor.

- Read the smart-contract audit reports — including the withdrawal flow. Ask: what auditors looked at the withdrawal path and bridge adapter, when, and was the report public? Anything that handwaves on this is auto-disqualified.

- Check the AVS opt-in list. Each LRT opts into a different set of AVSs (EigenDA, Lagrange, Witness Chain, AltLayer, etc), and each AVS has its own slashing rules. Ether.fi runs 10+. Puffer runs fewer with deliberately conservative selection. EigenLayer slashing has been live since April 2025 but no AVS has yet executed a slash event. That record will not stay clean indefinitely.

- Test the redemption queue before committing capital. Withdraw a small amount first. Lido stETH redemptions clear in 1–5 days; LRT redemptions can take 7–14 in normal conditions, and Kelp's were frozen for five weeks post-exploit. If you cannot tolerate the queue — or an indefinite freeze — the LRT is not suitable regardless of yield.

- Compute cash yield vs points yield. Headline "10% APR" usually decomposes into 3% base ETH staking + 1% AVS rewards + 6% points-implied value. Points value is speculative. ETHFI fell 96% from ATH to ~$0.38 by May 2026. Size positions on the cash yield only; treat any airdrop upside as a free option, not a return.

Realistic LRT portfolio (May 2026)

Sample $50k allocation: $30k weETH on Aave/Morpho (3.5% + collateral utility), $12k Pendle PT-weETH 3-month (5–6% fixed), $5k stETH baseline (depeg-resistant), $3k pufETH or ezETH for diversification. Last verified: 2026-05-27.

For a $50,000 ETH allocation seeking restaking exposure without overconcentration post-April 2026:

| Allocation | Position | Expected yield | Notes |

|---|---|---|---|

| $30,000 | weETH on Aave or Morpho (collateral) | 3.5% + borrow utility | Deepest DeFi acceptance; held through contagion |

| $12,000 | Pendle PT-weETH (3-month) | 5–6% fixed | No restaking exposure; locks in yield |

| $5,000 | Plain stETH (depeg-resistant baseline) | 3.0–3.4% | Zero LRT-specific risk |

| $3,000 | pufETH or ezETH (diversification) | 3.5% | Small satellite; monitor TVL recovery |

Rationale: Ether.fi dominance is now even more concentrated post-April 2026, making weETH overconcentration a protocol-specific risk to manage. Pendle PT locks yield without inheriting LRT smart-contract or bridge exposure. Plain stETH remains the cleanest ETH yield with the best historical risk record.

Risk summary

Smart-contract/bridge risk (Kelp $292M), depeg risk (ezETH ~78% depeg Apr 2024), AVS slashing risk (live but no events yet), points-yield illusion (ETHFI -96% from ATH), and EigenLayer governance centralisation. Last verified: 2026-05-27.

- Cross-chain bridge risk. The April 2026 Kelp DAO $292M bridge exploit is the canonical example of a risk category that the LRT market systematically underpriced: off-chain verifier compromise enabling phantom minting. LRT contracts compose with EigenLayer contracts, cross-chain bridge infrastructure, and AVS contracts — each layer adds attack surface. The Kelp exploit did not involve a code bug; it exploited a single-point-of-failure in off-chain infrastructure.

- Depeg risk. ezETH dropped to approximately $688 (vs ~$3,100 ETH, roughly 78% depeg relative to par) in April 2024 when Renzo's airdrop allocation triggered concentrated exits through thin Balancer and Gearbox liquidity. rsETH depegged to ~0.85 ETH after the April 2026 exploit before recovering to ~0.97 ETH via the DeFi United buyback. Any LRT held as leveraged collateral can trigger liquidations on a depeg without the protocol itself doing anything wrong.

- AVS slashing risk. EigenLayer activated slashing on mainnet April 17, 2025. As of May 2026, no live slash events have been executed by any AVS against any operator — Blockdaemon reported zero slashing events recorded across all time. But the infrastructure to slash is live, AVS adoption is expanding, and the first material slash event will re-price every LRT.

- Points-yield illusion. ETHFI fell from $8.53 ATH (March 2024) to ~$0.38 by May 2026 — a 96% drawdown. REZ and PUFFER governance tokens followed similar trajectories. Size positions on the cash yield only; treat airdrop upside as a free option with significant downside correlation to ETH market sentiment.

- EigenLayer governance centralisation. EigenLayer's protocol upgrades and AVS approval still flow through EigenFoundation. A governance attack or contentious upgrade would cascade through every LRT. This is the systemic tail risk the category has not yet fully priced.

- TVL concentration risk. Post-April 2026, Ether.fi holds an even larger share of LRT TVL. If a vulnerability emerges in Ether.fi specifically, the category has no effective second tier to absorb withdrawals.

The brutal truth about LRTs

Realised cash yield is 3.5–5% — only 50–150bps above plain stETH — while introducing bridge risk, slashing exposure, redemption queues, and governance tail risk; the April 2026 contagion event proved these risks materialise faster and more severely than the market priced. Last verified: 2026-05-27.

Realised cash yield in 2026 is 3.5–5% — only marginally higher than plain stETH at 3.0–3.4%. The differential comes from AVS reward streams that are still small and lumpy, plus token incentives that have largely disappointed (ETHFI -96% from ATH). The April 2026 Kelp exploit wiped out the equivalent of multiple years of LRT yield premium for rsETH holders caught in the 46-minute window before the pause — and Aave depositors collateralised against rsETH suffered a separate wave of bad-debt contagion. Use LRTs as a yield-enhanced satellite, not the core staking position. Cap LRT exposure at under 20% of total ETH holdings.

Looking ahead to 2027

Concrete signals to watch:

- EigenLayer slashing in production. Slashing infrastructure has been live since April 2025 with zero executions through May 2026. The first time an AVS slashes 1%+ of a restaker base, the category re-rates permanently. The clean record so far reflects AVS caution, not absence of risk.

- Kelp's CCIP migration. Whether Kelp successfully rebuilds credibility under Chainlink CCIP rather than LayerZero's 1-of-1 DVN architecture will determine if rsETH recaptures second-place TVL legitimately or if Ether.fi consolidates a near-monopoly.

- TVL recovery at Renzo/Puffer/Swell. All three saw 80–95% TVL declines. A return to pre-April 2026 levels would require both restored confidence and a positive risk appetite cycle in broader crypto. Neither is guaranteed.

- AVS revenue maturation. Right now AVS rewards are small relative to base staking. If EigenDA, Lagrange, or AltLayer cross $50M annualised fees paid to restakers, the cash yield differential vs LSTs widens enough to justify the risk premium on a pure yield basis. Until then, plain LSTs win on risk-adjusted return.

- Pendle PT dominance. PT-weETH accounts for a growing chunk of weETH supply. If institutional capital continues preferring the fixed-yield wrapper, the LRT issuers hold the slashing/bridge risk while Pendle holders take the yield — economically disintermediating the LRT issuers over time.

Related: How to Stake ETH · Best Liquid Staking Tokens 2026 · What Is Restaking / EigenLayer

Frequently asked questions

What is restaking?

Restaking lets you reuse staked ETH (or LSTs like stETH) as collateral to secure additional services on top of Ethereum — oracle networks, bridges, data availability layers, and L2 sequencers (collectively called Actively Validated Services, or AVSs). EigenLayer pioneered this model. You earn extra yield on top of base ETH staking but take on additional slashing exposure.

What is a Liquid Restaking Token (LRT)?

An LRT is a tokenised receipt for restaked ETH — eETH (Ether.fi), ezETH (Renzo), rsETH (Kelp), pufETH (Puffer), rswETH (Swell). Like LSTs, you can use them as collateral in DeFi while still earning restaking rewards. Five LRTs once controlled 96% of restaking market share, but the April 2026 Kelp exploit triggered severe TVL contractions at Puffer, Renzo, and Swell.

What is the largest restaking protocol in 2026?

Ether.fi leads with $3.8B TVL as of May 2026 (DefiLlama). Kelp DAO is second at $1.35B (recovering post-hack). Renzo, Puffer, and Swell all saw catastrophic TVL declines following the April 2026 Kelp bridge exploit and resulting sector-wide contagion. EigenLayer (the base layer) holds ~$8.9B in restaked ETH (March 2026 data, down from an $18B+ peak).

Are LRTs safe?

LRTs add three risk layers on top of holding ETH: (1) base staking slashing, (2) AVS slashing once enabled, (3) smart-contract and bridge/infrastructure risk in the LRT and EigenLayer contracts. The April 2026 Kelp DAO $292M bridge exploit — attackers compromised a single LayerZero verifier node (1-of-1 DVN setup) to mint unbacked rsETH — triggered massive withdrawals across the category and remains 2026's largest DeFi theft. LRTs are not stETH-equivalent in risk.

How much yield do LRTs pay?

Base ETH staking yield (~3.0–3.4%) + AVS rewards + protocol points/airdrops. Realised cash yield in 2026 sits at 3.5–5% on most LRTs; points add speculative upside via future token airdrops. Headline 10%+ APYs typically include token-emission incentives that may not persist. ETHFI's governance token fell from an $8.53 ATH (March 2024) to ~$0.38 by May 2026, illustrating how airdrop upside often disappoints.

What is an AVS?

Actively Validated Service — any protocol that uses restaked ETH for cryptoeconomic security. Examples: EigenDA (data availability), Lagrange (ZK coprocessor), Witness Chain (proof-of-location), AltLayer (rollup-as-a-service). Each AVS pays restakers in fees or its own token; each adds its own slashing conditions. EigenLayer has 20+ AVSs live and ~1,900 active operators as of early 2026.

What's the difference between EigenLayer, Symbiotic, and Karak?

EigenLayer is the largest by TVL (~$8.9B as of March 2026) and pioneered the AVS model — restaked ETH secures third-party services in exchange for additional yield. Symbiotic is permissionless (anyone can deploy a network) and supports any ERC-20 as collateral, not just ETH and LSTs. Karak takes a similar permissionless approach with broader asset support. EigenLayer dominates on AVS variety; Symbiotic and Karak compete on flexibility.

How much extra yield does restaking actually pay in 2026?

AVS rewards in EIGEN, AVS-native tokens, and points typically translate to 1–2% additional APY on top of base ETH staking yield (~3.0–3.4%). Total LRT yield in 2026 runs 4–5% gross, before fees and slashing. The headline "restaking pays 10%+" numbers from 2024 were largely point-program farming that wound down post-token launches. No major AVS has yet generated slash events on EigenLayer mainnet (slashing went live April 2025) — so the incremental yield is real but thin.

What happens if I get slashed on a restaked LRT?

You lose principal proportional to the slashing event, allocated across all LRT holders unless the LRT issuer maintains an insurance buffer. Ether.fi, Renzo, Puffer, and Kelp have different slashing-coverage policies — some absorb the first percentage of loss, others pass through directly. As of May 2026, no EigenLayer AVS has executed a live slashing event, but the infrastructure to do so has been live since April 2025.

Should I use an LRT or restake directly?

LRT for liquidity and convenience; direct restake for control. LRTs abstract AVS selection and pay you a tradeable token that earns yield passively. Direct restaking through EigenLayer or Symbiotic lets you pick AVSs individually but requires active management and lacks liquid exit. After the Kelp exploit highlighted bridge/infrastructure risk as a third attack surface, the calculus shifted: direct restaking on EigenLayer avoids LRT-specific bridge risk but inherits AVS slashing risk directly.

Sources & further reading

- DefiLlama — Ether.fi TVL (live)

- DefiLlama — Kelp TVL (live)

- DefiLlama — Puffer Finance TVL (live)

- DefiLlama — Renzo TVL (live)

- DefiLlama — Swell Liquid Restaking TVL (live)

- Chainalysis — Inside the KelpDAO Bridge Exploit (April 2026)

- CoinDesk — Kelp DAO exploited for $292 million (April 19, 2026)

- CoinDesk — Kelp claims LayerZero approved the setup blamed for hack (May 5, 2026)

- CryptoTimes — Aave and Kelp DAO restore rsETH operations (May 26, 2026)

- CoinDesk — EigenLayer adds slashing feature (April 17, 2025)

- Fensory — EigenLayer TVL restaking analysis March 2026

- Cointelegraph — Renzo ezETH depegs to $688 (April 2024)

- EigenLayer official docs (EigenCloud)

- Ether.fi documentation

- Pendle Finance — fixed-yield LRT markets